Alantra: Finance at a Reasonable Price

Introduction

Alantra is a Spanish financial services provider with offices in 19 different countries. The company operates in two key divisions, asset management, and financial advisory, with the latter being the key driver of profitability on a normalized environment.

The overall M&A market has been under severe pressure over the last few years on the back of the rising interest rate environment, which has paralyzed deal-making activity across the globe. Alantra is specifically focused on the mid-market, which remains in the doldrums (although activity among larger companies has already started to pick up). Going forward, declining interest rates should provide a tailwind to overall dealmaking activity.

Alantra is sitting on a rock-solid position, with almost ~€150M in net cash and investments on the balance sheet (equating almost half of the company’s current market capitalization). Furthermore, the company owns minority interests in a myriad of financial operators with a book value of €80.9M as of Q3-end (which likely understates the market value of Alantra’s stakes).

Overall, the downside from current pricing appears limited considering the company’s solid financial position and growing asset management business. However, profitability is likely to remain under severe pressure until M&A activity picks up in the mid-market, so the opportunity risk is a key factor to be on the lookout for if the recovery is pushed further into the future.

Financial Advisory: Investment Banking & FIG

The financial advisory side of the business, which currently includes both investment banking and FIG, is Alantra’s key profit center. The sector is currently in a severe downturn, as rising interest rates have ground the sector to a halt. For instance, revenues for Q1/Q3-24 more than halved relative to the same period in 2021 (€63.2M vs €136.4M respectively). FIG performance has also been under pressure, down 35.5% during the same timeframe (€21.6M vs €33.5M). Interestingly, performance on the financial advisory side segment has steadily deteriorated over the past three years, with revenues (and profits) down sequentially since 2021 through to the current year.

The magnitude of the current downturn likely points to a swift recovery. Rising interest rates dented activity over the last few years, particularly among private equity players (which are unlikely to capture operational synergies from M&A transactions), creating pent-up supply (and demand) for when interest rates decline.

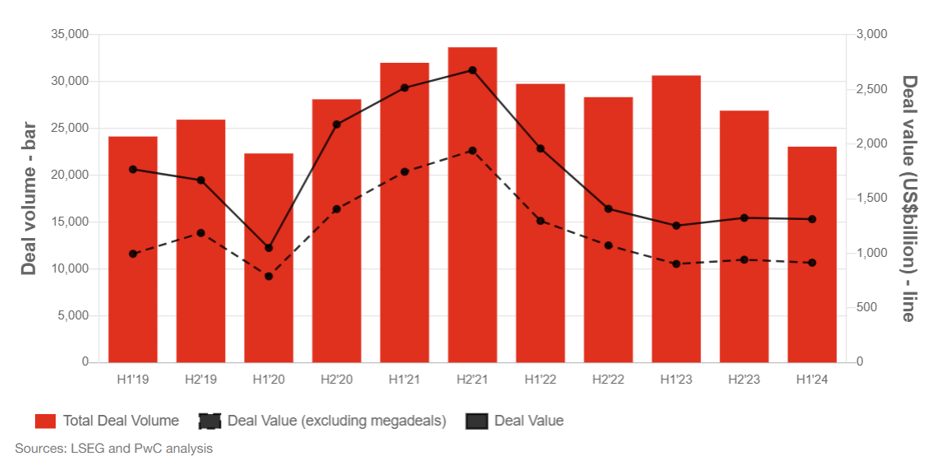

As illustrated in the image below (I strongly encourage reading Brian Levy’s piece, although it is now a few months old), albeit total deal value has stabilized over the past couple of years total deal volume (i.e., the number of deals) has consistently declined (which essentially means that dealmaking in the small/mid-market has continued to soften).

Source: Global M&A Industry Trends, Brian Levy for PwC.

Overall, predicting when the market will turn is anyone’s guess, but a declining interest rate environment should provide a tailwind all-else equal. Furthermore, pent-up supply/demand among private equity players is likely to be significant, especially as funds mature (and new equity is raised elsewhere).

Asset management

Alantra also has an asset management arm, which as of Q3-end, managed €2.462M, broken down as illustrated in the image below (FAUM stands for fee-earning assets under management, whereas AUM stands for assets under management). Core earnings on this side of the business are significantly more stable than on the investment banking side, since they usually charge a percentage of AUM, although success fees (or the carried interest) tend to be far more volatile from one quarter to another, since it is contingent on realizing the gains on a specific fund.

Source: Alantra’s Q3 earnings presentation, slide 12.

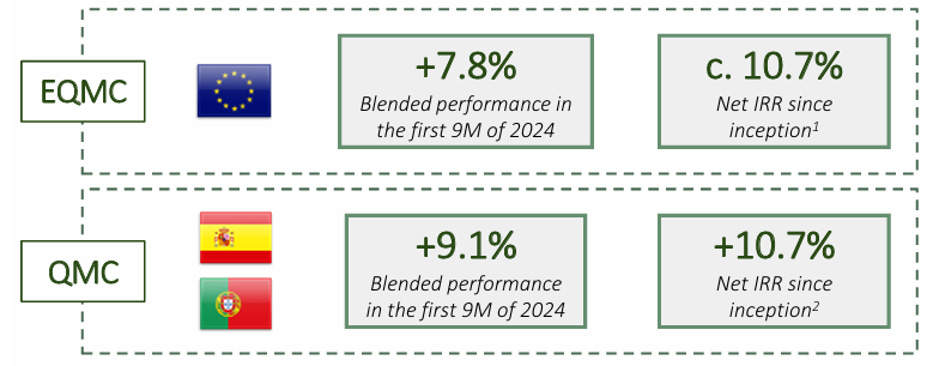

The company’s flagship public equity funds, the EQMC and the QMC have performed remarkably well since inception, with a net IRR of 10.7% since January 2010 and July 2013 respectively. The EQMC focuses in the “pan-European listed small and mid-cap space”, with an active strategy involving taking significant minority positions in a “concentrated portfolio of 12-16 companies”. The QMC takes a similar approach in the Iberian market (Spain & Portugal).

Source: Alantra’s Q3 earnings presentation, slide 12.

Overall, the asset management business generated a net profit of €5.3M throughout the first half of the year (the company is only obligated to provide its full financials on a semi-annual basis). Considering asset management businesses tend to carry steep valuations (15x+ earnings), this is a significant value driver for Alantra. Overall, assuming normalized net income of ~€10M (which should be on the conservative side considering it came in at €11.1M last year), and using a 16x multiple, this segment alone should be worth ~€160M for Alantra.

Minority Interests

Alantra also owns stakes in a myriad of operators in the overall financial ecosystem. These are not consolidated on Alantra’s financial statements but have become sizable profit centers (and cash generators by dividend distributions to the parent) over the past couple of years. Between Q1 and Q3-24, Alantra recognized €7.5M in profit using the equity method from its investees, a sizable improvement from 2023’s €4.3M in the same period.

As illustrated in the image below (from the H1-24 financial statement), the largest value drivers are Access Capital Partners Group, Singer Capital Markets, and AMCHOR Investment Strategies. Access Capital Partners is a pan-European private equity outfit managing both funds of funds and direct funds; Alantra acquired its stake for €43.5M in two tranches, and Access is likely more valuable now (although I do not have specific insights on their financials and outlook).

Source: Alantra’s H1-24 financial statement.

Singer Capital Markets is a UK investment bank providing both investment banking services while also being a top liquidity provider for the overall UK stock market (with a 10% market share on AIM throughout 2023). AMCHOR is an asset management outfit focused on private equity.

Valuing Alantra’s stakes in these smaller outfits is no easy feat given the limited amount of publicly available information on most of these companies. I believe a reasonable starting point is the book value of these investments on Alantra’s balance sheet, which stood at €80.9M as of Q3-end, but this is likely on the conservative side, especially once the market starts to recover.

Financial Position, Valuation & Catalysts

Alantra sits on a rock-solid financial position, with €78M in cash and cash equivalents, €27.9M invested in a monetary fund, and €44M invested across an array of products managed by the Group as of Q3-end. The company has no debt on its books, whereas total liabilities are also quite limited.

At current pricing, Alantra has a market cap of ~€300M. The company’s net cash position (including investments) stood at €149.9M; assuming €50M are required to manage the overall business (which is unlikely considering some peers do have debt on the capital structure), that would leave ~€100M directly attributable to shareholders on top of the other existing businesses.

The asset management side of the business can be valued at €160M using a somewhat conservative multiple, especially if they manage to continue delivering on the operational front, realizing a solid IRR on their funds). The minority interests accounted for using the equity method can be valued at book value, i.e., €80.9M as of Q3-end.

Finally, we have the investment banking side, which I believe should be worth around 10x normalized earnings. Estimating what normalized earnings are on this side of the business is no easy feat, but the number likely stands at around €15M-€20M (~€17.5M at the midpoint; applying a 10x multiple given the cyclicality of the business, that would amount to around €175M).

This would lead to the following valuation:

- €100M in net cash

- €160M for asset management

- €80.9M in minority interests

- €175M for the investment banking outfit

Total: €515.9M, or ~€13.49/sh for ~69% upside from current pricing.

Overall, I believe these estimates are likely on the conservative side, especially considering the fact that when the market turns, sentiment will likely improve, potentially leading to higher multiples and thus overall valuations/pricing.

The main risk I see at current pricing is significant opportunity cost if the recovery on the investment banking side of the business is delayed further into the future, since, in my opinion, that is the most obvious catalyst. Management could also sell one of their minority stakes at solid pricing and declare a special dividend with the net proceeds or execute a tender offer (at current pricing I favor share repurchases, but trading volume is so anemic it would take a while to repurchase a meaningful number of shares, so a tender offer seems more appropriate).

Conclusion

Alantra is trading at a heavily discounted valuation despite being a solid operator with a good track record. Downside from current pricing appears limited barring a black-swan event, but upside is contingent on an improving backdrop for the investment banking side of the business (especially on the mid-market); however, if the M&A trends improve, upside is significant, providing an interesting opportunity on a risk-reward basis.

The asset management outfit remains a key value driver for the company, and continued growth on that business is contingent on solid performance on their funds (both public and private), although the IRR since inception has been remarkably solid (especially considering how the Iberian market has fared over the past decade).

Overall, I believe now is the time to start following the company. I have started to build a position and will likely buy more if the mid-market starts to recover and share pricing lags behind the recovery. Given the company’s historical dividend policy (they tend to distribute ~100% of net income), it is unlikely that share pricing will severely lag a recovery in earnings. For further information on the company, I recommend reviewing these two writeups (in Spanish): I and II.

I am long Alantra.