Global Dominion: Services Provider with an Infrastructure Kicker

Introduction

Global Dominion is a Spanish publicly traded company with a market cap of ~€430M. DOMI is a services provider as well as an EPC (engineering, procurement, and construction) contractor. Furthermore, the company also owns several renewable energy projects (mostly photovoltaic in Latin America). The company used to operate in a net cash position, but the development of the pipeline of renewable energy infrastructure has ultimately led to higher leverage, whereas the contribution from the aforementioned assets has so far been somewhat lackluster.

DOMI was spun-off from CIE Automotive in 2016. The company was initially created in 1999, with the objective of providing in-house technology consulting to improve efficiency and generate savings. Since going public, DOMI has expanded its offering, and over the past few years has increasingly focused on services related to the energy transition (including waste management among others).

Management is now focused on simplifying the company’s structure while delivering on their 2023-2026 strategic plan. I believe that the sale of certain of their renewable infrastructure assets should have a positive impact on earnings due to reduced financial expenses (most of the company’s debt is tied to those projects) while significantly reducing the company’s overall enterprise value, solidifying the low multiple the company is currently trading at. Insiders have skin in the game, with the President of the company owning a 5.7% stake, the CEO owning 5.8%, whereas CIE Automotive insiders own 15.2% of the company.

Business Lines

The company operates in three differentiated business lines:

· Sustainable Services

· 360 Projects

· Renewable Infrastructure

The company previously operated another business line named B2C (business to consumer), where they operated as a commercial retailer of gas/electricity/telecom services (among other things) via the commercial outreach of the Phone House, which they acquired in 2017. However, they ultimately decided to winddown the operation given the mediocre economics they were generating. B2C was integrated into the sustainable services division throughout the winddown of the former.

Sustainable Services

This segment currently represents the majority of the company’s revenues and profit (73% of the sales and 64% of the operating profit excluding renewables infrastructure). 2024 to date, revenues increased 3%, although organic growth was far stronger, coming in at 8%, offset by a -1% forex impact and by -4% inorganic growth due to the restructuring of the B2C segment.

However, operating profits from the segment increased 19.2% y/y, with the margin jumping to 12.6% of revenues on the back of the restructuring of the retail business, which had inherently lower margins. Going forward, management expects margins to increase as they continue to shift the business mix of the segment to the circular economy.

This segment is characterized by consuming working capital, although on the other hand, CAPEX is almost non-existent on this side of the business. Management targets recurring contracts to cover 85% of revenues and a contribution margin of ~12% (which has so far been achieved year-to-date).

In the image below, some of the services DOMI provides under the Sustainable Services division are illustrated. The company has worked since 2019 in the O&M of electrical lines in South America (Chile, Colombia, and Peru), has become a “one-stop-shop” for a very large chemical manufacturer in Spain, and has worked on digitalizing companies to make them more efficient.

Source: November Corporate Presentation, slide 26.

DOMI’s shift towards “sustainable services” is also illustrated by the acquisition of Gesthidro, specialized in recycling and industrial residue cleanup (the transaction closed in 2023, with DOMI acquiring the 49% that was not yet owned by them). Furthermore, DOMI recently closed the sale of their Spanish industrial maintenance services unit to the Serveo Group for €28.8M (which will generate an after-tax capital gain of approximately €11.6M net to Dominion). The multiple paid by the Serveo Group was around 6x EBITDA, since turnover and recurring EBITDA amounted to €105M and €4.8M respectively (per management’s commentary).

Going forward, we believe it is reasonable to expect sustainable services to continue growing organically by around 5-10% with margins also increasing slightly. The issue with this side of the business is that it is difficult to exactly pinpoint the underlying drivers of profitability (management providing some additional insight would be helpful), but industrial activity should be a reasonable proxy.

360º Projects

Through this segment, DOMI provides engineering, procurement, and construction services to its clients. The company provides all the required services (hence the 360º), which allows DOMI to capture margins across the value chain (while also striving to secure the subsequent operations & maintenance contracts), which provide more recurrent revenues.

This segment tends to generate working capital (as DOMI strives to get prepayments), has solid margins (2024-to-date it has generated a 19.1% contribution margin), and has a fairly stable backlog, with DOMI finishing Q3 with a backlog of €628M. DOMI usually provides the breakdown of the orderbook between industrial, renewable, or social infrastructure (hospitals, etc.), but they did not in Q1, which makes comparisons more difficult.

Source: Own elaboration based on company filings. Q1-24 figure estimated to be down slightly relative to Q4-23 (management mentioned it was “stable” q/q).

Order intake from the renewables side of the business has been lackluster since mid-2023 on the back of the elevated interest rate environment, which weighs on the economics of renewable energy projects (long-lived assets with large upfront costs tend to require of significant amounts to debt to generate decent IRRs).

However, despite the slower intake on that side of the business, the company has managed to generate solid intake from both industrial and social infrastructure projects, while also keeping the contribution margin of the segment at elevated levels (management has been clear they are not willing to sacrifice margins in exchange for more projects).

Interestingly, the contribution margin for the 360º business is running above management’s long-term target, set at 15%, although they have also cautioned that the 15% target is kind of a “low bar”, and they have historically managed to run well above that number (the contribution margin averaged 18%, 18.3%, and 19.3% during 2021, 2022, and 2023 respectively).

Some activities pursued under this division are included below, namely the design, construction, and O&M contract for the development of a 78MW photovoltaic park in the Dominican Republic, the technological integration and O&M in hospitals in Antofagasta (Chile), and the design, construction, and O&M of two warehouses for pellets for a client transforming a power plant into a biomass plant.

Source: November Corporate Presentation, slide 27.

Although this is a highly competitive industry, DOMI has historically been able to operate with reasonable margins. The slowdown in the renewable energy space has weighed on growth, but they have managed to maintain profitability at very elevated levels. The backlog is now sitting at €628M, providing significant visibility into 2025.

Renewable Infrastructure

Global Dominion decided a few years ago that not only would they provide services to the renewable infrastructure players, but that they would take ownership stakes in certain projects if the numbers made sense. In late-2021, Incus Capital entered this division by acquiring 23.4% of the firm for €50M (€214M equity valuation). However, Global Dominion subsequently agreed to acquire Incus Capital’s stake for €66.9M (for an equity valuation of €286M).

DOMI’s stakes in infrastructure projects are illustrated in the image below. Most are in the renewable energy sector, but the company also owns a 15% stake in the Antofagasta hospital and a 10% stake in the Buin Paine hospital; the former is already operating, whereas the latter is still under construction. Both assets are operated alongside Sacyr, a large Spanish infrastructure owned and developer. Valuing these stakes in no easy feat, so I believe it is reasonable to take book value as a starting point (which is likely on the conservative side); this would amount to a combined €6.6M as of Q2-end (€5.127M for the Antofagasta stake and €1.438M for the Buin Paine participation).

Source: Global Dominion’s Q3 Earnings Presentation, slide 7.

The earnings and FCF contribution from this segment has been severely affected by the rising interest rate environment, whereas DOMI has been slow getting projects online. For instance, the Cerritos wind farm (located in Mexico) has been held for sale for well over a year, and it seems it has yet to operate at capacity; in mid-2023, DOMI mentioned they were very close to closing the sale of the Cerritos wind farm, which was awaiting the government’s authorization to sell the electricity produced, but it seems DOMI still has not received that, although alongside Q3 earnings, the company mentioned the park was energized and “working on the permitting for its imminent startup” (page 12 of the following document).

Overall, most of the value of this segment comes from the company’s ownership in the Cerritos windfarm as well as the projects in the Dominican Republic (which are 50% owned, and some of which are already operational, and others are under construction or development). For instance, the Cerritos windfarm (once it has all the necessary governmental permits) could be sold for circa €90M (assuming €1.3-1.4M per MW, which seems reasonable even factoring Mexico as a jurisdiction).

Financials & Valuation

DOMI used to carry an exceptionally clean balance sheet, with a net cash position. However, that has changed over the past few years as they have built up their infrastructure business, which is very capital intensive (and has therefore led to higher leverage levels). All in all, indebtedness remains very manageable (with net debt below 2x EBITDA), but it has weighed on EV/EBITDA metrics, especially since the contribution from the infrastructure business has so far been fairly limited (they are investing in greenfield projects).

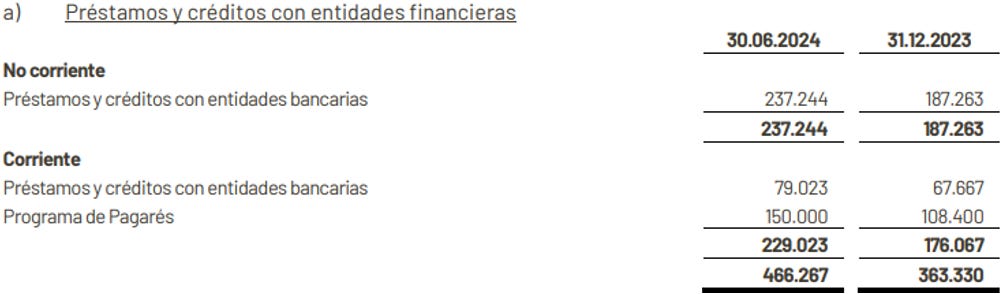

The company finished Q2 with a net debt position of €198.1M, composed of €466M in total gross debt minus €164.1M in cash and cash equivalents minus €104M in other current financial assets (the company also had €10.1M in non-current financial assets, but those were not included in the net debt calculation).

Source: Global Dominion’s H1-24 Results, page 18.

The company’s debt breakdown between current and non-current can be seen in the excerpt below. DOMI’s indebtedness has increased materially y/y as they paid €76M for inorganic growth, spent €20M in CAPEX, whereas the winddown of the B2C business resulted in a €40M negative impact to working capital (the beauty of retail is that cash comes in before it goes out, so customers arguably finance activity for free).

Source: Global Dominion’s H1-24 Results, page 39.

However, those figures do not include the debt associated to the assets held for sale, which is significant for the Cerritos wind farm, which had €80M in debt as of Q2-end. Therefore, the company’s “real” net debt position amounted to closer to €278M, for an EV of almost €700M at current share pricing.

Source: Global Dominion’s H1-24 Results, page 57.

However, I believe we should deduct the €28.8M in net proceeds from the sale of the Spanish industrial maintenance services unit to the Serveo Group, a €15M placeholder for Q3 FCF, and around €90M for the sale of the Cerritos windfarm from EV. Under those assumptions, and assuming an annual EBITDA of around €145M (€150M minus around €5M from the Spanish industrial maintenance services unit), the company is currently trading at an EV/EBITDA of ~4x.

However, the Cerritos windfarm does move the needle on the valuation front, since if it remain a stranded asset (i.e., no FCF generation) and is not sold, the EV/EBITDA multiple would increase to 4.5x. Assuming €145M in EBITDA this year may be a bit aggressive (but I believe this assumption to be reasonable), and illustrates that DOMI is not delivering on their 2023-2026 strategic plan; their 2023 target was for EBITDA of €150M and Operating FCF of €70M+, and through H1-24 they had only generated €71.3M and €25M respectively). Per their targets, the company’s EBITDA and operating FCF should have been €160.5M and €76.3M respectively.

Source: November Corporate Presentation, slide 15.

Conclusion

DOMI is trading at a very cheap valuation, there is no question about it, especially considering that part of the EBITDA is generated by infrastructure assets, which are usually valued at strong multiples. However, the company has not delivered well over the past year, with the Cerritos windfarm weighing on results (although since they account for it as an asset held for sale the impact is sometimes not apparent).

Since the company is continuously pursuing M&A activity, y/y comparisons become tricky, especially since management provides specific commentary on how growth fared organically and inorganically (while also talking about one-offs), making comparisons over the years difficult. Going forward, and after the exit of the B2C segment, comparability should improve.

Returns on the renewable infrastructure side of the business have, so far, been lackluster. The company’s implied cost of equity is currently too high to justify investing in additional projects, with share repurchases offering a more compelling risk-reward (at least on paper). Furthermore, the delays on the sale of the Cerritos windfarm (and the little commentary management has provided) is somewhat concerning; delays in securing government approvals are a headache, but I believe management should be more straightforward with the market (especially considering the amount of capital invested in that asset).

Looking ahead, I expect management to opportunistically sell the Cerritos windfarm as well as the photovoltaic parks in the Dominican Republic, which should have a very positive impact on the company’s balance sheet (if those transactions materialize I expect the company’s net debt position to plummet, which should also lead to higher FCF due to the reduced interest burden), providing significant flexibility to pursue more aggressive share repurchases.

I’m long DOMI, but it’s a small position for now. I plan to add more shares if we get some visibility on the divestment of their renewable infrastructure assets (management intends to be net debt €0 by 2026, which almost assuredly implies the sale of these assets going forward). DOMI’s management has historically delivered well; they were caught wrong-footed by the rise in interest rates, but I believe this too shall pass.